Market Outlook

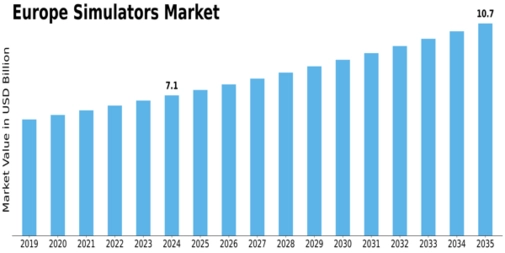

Forecasts indicate the Europe simulators sector will grow from USD 7.08 billion in 2024 to roughly USD 10.7 billion by 2035 at a ~3.83% CAGR. These figures underscore a steady expansion rather than explosive growth, yet the decisive factor will be competitive differentiation and innovation among market players.

Industry Overview

The market covers a broad spectrum: aerospace and defence training simulators, industrial and manufacturing process simulators, maritime and land vehicle simulators, and emerging gaming or synthetic-environment simulation. The convergence of training, safety, cost-control and digital transformation themes positions the simulation market as a strategic domain rather than a niche segment.

Key Players

Key firms mentioned in the MRFR report include Thales Group, Siemens AG, Boeing Company, Kongsberg Gruppen ASA, Northrop Grumman Corporation, FlightSafety International and CAE Inc. Additionally, global intelligence indicates firms such as L3Harris Technologies, Rheinmetall AG, Indra Sistemas SA and Saab AB operate in the broader simulation space targeting Europe.

What stands out is that these companies bring strong legacy capabilities (especially in defence or aviation) but are increasingly turning to advanced techniques such as virtual reality, synthetic training environments, digital twins and immersive simulation to drive differentiation.

Segmentation & Strategic Implications

- By type and platform: Companies offering full-flight or full-motion simulators (for aviation) must compete on fidelity, certification, cost and service. Meanwhile, providers in land/maritime or industrial domains may compete on modularity, software integration and flexibility.

- By solution: Firms that bundle services—maintenance, upgrades, training packages—gain advantage as customers shift to service-oriented models.

- By technique: Use of VR/AR, synthetic environment simulation and gaming-based simulation is a key differentiator. Those firms who can deliver immersive, cost-effective training solutions will likely capture market share.

- Regional insight: Germany leads the European region, supported by strong industrial, aerospace and defence sectors. UK, France, Italy, Spain also offer opportunities. Market entrants should consider regional regulatory compliance, local training needs and government funding initiatives.

Conclusion

For companies operating inEurope simulators market, success will depend on more than simply launching new hardware. It will be about offering integrated, immersive, cost-effective simulation solutions aligned with target sectors. Firms that innovate on technique, vertical application and service models stand to gain the most as the market grows steadily.